Predicting the XAU-USD Foreign Exchange Prices

Overview

This was a final project output for our Machine Learning course under Prof. Chris Monterola in the M.Sc. Data Science program. We used actual hourly price data from a foreign forex broker to predict the gold price. Various machine learning models were explored and a trade simulation was ran using the last 6 months of the dataset. The simulation from our best model resulted to a 54% return on investments. This study was presented to the public last August 2019.

Report

Foreign exchange (forex) is the largest financial market in the world with a daily average of \$5 trillion each day versus the largest stock market, New York Stock Exchange, which averages to \$75 billion only. Forex is a decentralized market, meaning there is no single physical location where investors go to buy or sell currencies. Individuals or retailers can trade forex anywhere and anytime through their laptops or phones. Forex provides favorable leverage that a small amount of money can be used on large trades. This market is the most volatile yet has the highest return possible as well. However, since we don’t live in a perfect world, it has the highest risk of losing money as well. One of the most explored foreign exchange problems is the prediction of forex prices (determining whether it will go up or down) of different currency pairs. This is a classification problem with binary values as outputs. Another obvious approach would be to treat it as a time series data. However, this requires working under the assumption that the data is linear and stationary - which is not true for forex prices. Financial time series are inherently noisy and unstable that it is tough to enhance forecasting accuracy.

For this study, a classifier which predicts direction of trades is employed. Our classifier will recommend a trade (class 1) if in the next four hours the forex price is predicted to reach at least 300 pips higher than the previous closing price. Otherwise, the classifier will not recommend a trade (class 0). A pip or “percentage in point” computes the gains or losses of every trade. It is the unit of change in a currency pair - the smallest price change that a given exchange rate can make.

Machine Learning Packages

import sklearn

from sklearn.linear_model import LogisticRegression

from sklearn.svm import LinearSVC

from sklearn.tree import DecisionTreeClassifier

from sklearn.ensemble import RandomForestClassifier, GradientBoostingClassifier

from sklearn.preprocessing import StandardScaler, MinMaxScaler

from xgboost import XGBClassifier

from sklearn import metrics, model_selection

from sklearn.model_selection import GridSearchCV, train_test_split

Sample Data

| open | high | low | close | volume | ceiling | floor | ma_short | ma_short2 | ma_mid | ma_long | trigger | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| datetime | ||||||||||||

| 2015-09-10 01:00:00 | 1106.40 | 1107.52 | 1106.06 | 1107.06 | 775 | NaN | NaN | 1107.470000 | NaN | NaN | NaN | NaN |

| 2015-09-10 02:00:00 | 1107.07 | 1107.91 | 1106.93 | 1107.81 | 414 | NaN | NaN | 1107.583333 | NaN | NaN | NaN | NaN |

| 2015-09-10 03:00:00 | 1107.81 | 1108.32 | 1106.28 | 1107.18 | 1081 | NaN | NaN | 1107.448889 | NaN | NaN | NaN | NaN |

| 2015-09-10 04:00:00 | 1107.23 | 1107.23 | 1103.87 | 1106.81 | 2739 | NaN | NaN | 1107.235926 | NaN | NaN | NaN | NaN |

| 2015-09-10 05:00:00 | 1106.81 | 1107.72 | 1106.12 | 1106.93 | 1517 | NaN | NaN | 1107.133951 | NaN | NaN | NaN | NaN |

The dataset contains actual hourly prices from Sep 10, 2015 to June 15, 2018 for a total of 16,298 observations/rows. The raw features were the open, high, low, and close prices and the volume.

datetime - Year/Month/Day/Hour

open - opening price within the hour

high - highest price within the hour

low - lowest price for within hour

close - closing price within the hour

volume - number of trades within the hour

Other indicators were also calculated from these raw features:

ceiling - highest price of the day before

floor - lowest price of the day before

ma_short - moving average for a certain number of days (Non-Disclosure Agreement)

ma_short2 - moving average for a certain number of days (Non-Disclosure Agreement)

ma_mid - moving average for a certain number of days (Non-Disclosure Agreement)

ma_long - moving average for a certain number of days (Non-Disclosure Agreement)

trigger - a certain technical indicator (Non-Disclosure Agreement)

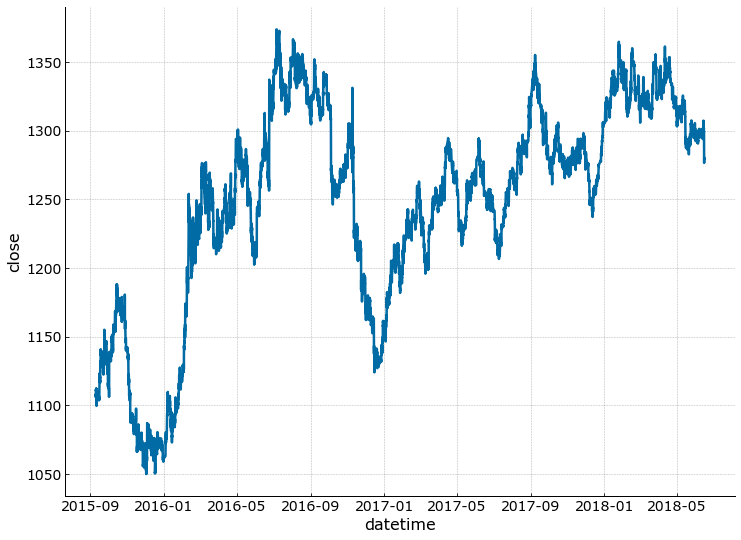

Exploratory Data Analysis

It can be observed that the whole dataset is on an upward trend but mostly ranging with numerous dips. Gold price was ranging since the reversal in 2011 up to 2018.

Methodology

Before modeling, we calculate the proportional chance criteria (PCC) for the dataset. This is the proportional by chance accuracy rate which computes the highest possible random chance of classifying data without explicit mathematical model other that population counts. As a heuristic or rule of thumb, a classifier machine learning model is considered highly succcesful when the test accuracy exceeds 1.25*PCC.

def pcc(y, factor=1.25):

"""

PARAMETERS

----------

factor: float

Applied factor to the Pcc to determine target test accuracy

RETURNS

-------

pcc: float

The proportional chance criteria

"""

counts = np.unique(y, return_counts=True)[1]

num = (counts/counts.sum())**2

pcc = 100*factor*num.sum()

return pcc

Setting up the features

We cannot directly use the features for modelling since they will cause the model to predict the forex trend using features that are in the same time period. Instead, we generated features for modelling from the lagges values of the orginal features.

- 21-hour lag window

- moving averages

- trigger*

highest attainable price in the next 4 hours

*confidential information from data source / broker

def generate_features(df, window_range=5):

""" Generate features for a stock/index/currency/commodity based on

historical price and performance

PARAMETERS

----------

df : pandas DataFrame

dataframe with columns "open", "close", "high", "low", "volume"

window_range: int, optional (default=5)

lagged time to include in the features

RETURNS

-------

df_new : pandas DataFrame

data set with new features

"""

df_new = pd.DataFrame(index=df.index)

# original features lagged

for window in range(1, window_range+1):

df_new[f'open_lag_{window}'] = df['open'].shift(window)

df_new[f'close_lag_{window}'] = df['close'].shift(window)

df_new[f'high_lag_{window}'] = df['high'].shift(window)

df_new[f'low_lag_{window}'] = df['low'].shift(window)

df_new[f'vol_lag_{window}'] = df['volume'].shift(window)

# special features

df_new['trigger'] = df['trigger'].shift(1)

df_new['ema_lagged'] = df['ma_short'].shift(1)

# average price

df_new['MA_5'] = df['close'].rolling(window=5).mean().shift(1)

df_new['MA_21'] = df['close'].rolling(window=21).mean().shift(1)

# average price ratio

df_new['ratio_MA_5_21'] = df_new['MA_5'] / df_new['MA_21']

# standard deviation of prices

df_new['std_price_5'] = df['close'].rolling(window=5).std().shift(1)

df_new['std_price_21'] = df['close'].rolling(window=21).std().shift(1)

# standard deviation ratio of prices

df_new['ratio_std_price_5_21'] = (df_new['std_price_5']

/ df_new['std_price_21'])

df_new = df_new.dropna(axis=0)

# targets, check the highest gold price attained in the next 4 hours

highs = df['high'].rolling(window=4).max().shift(-4)

df_new['high_close_diff'] = highs - df['close'].shift(1)

return df_new

data = generate_features(df, window_range=21)

Setting the targets

Target is an increase of 300 pips (\$3) in the next 4 hours. An additional 30 pips (\$0.3) is added to account for the difference in buying and selling prices. The difference is the spread for the forex brokerage.

def reco(x):

if x.high_close_diff > 3.3:

return 1

else:

return 0

data['target'] = data.apply(reco, axis=1)

targets = data['target']

X = data.drop(['target', 'high_close_diff'], axis=1)

Splitting the data into train-test

Even if the model built was a classifier, the data was split based on time periods. This ensures that the model is trained without seeing data from the future.

startDATE = datetime.datetime(2015, 9, 11, 1)

testDATE = datetime.datetime(2018, 1, 18, 1)

X_train = X.loc[startDATE:testDATE]

y_train = targets.loc[startDATE:testDATE]

X_test = X.loc[testDATE:]

y_test = targets.loc[testDATE:]

X_train.shape, X_test.shape, y_train.shape, y_test.shape

((13795, 113), (2420, 113), (13795,), (2420,))

We calculated the PCC of the dataset without sampling. It can be observed that the dataset is unbalanced with class 1 as minority. To address this, we use a sampling method called SMOTE (Synthetic Minority Oversampling Technique) to oversample the data for the purpose of balancing the classes.

pcc(y_train)

54.0

np.unique(y_train, return_counts=True)

(array([0, 1]), array([8906, 4889]))

Performing SMOTE

from imblearn import over_sampling

sampler = over_sampling.SMOTE()

X_sampled, y_sampled = sampler.fit_resample(X_train, y_train)

np.unique(y_sampled, return_counts=True)

(array([0, 1]), array([8906, 8906]))

Various Classifier Models

The models considerd for the classification are the following:

a. Logistic Regression (L2 Regularization)

b. Linear Support Vector Machine (L2 Regularization)

c. Random Forest Classifier

d. Gradient Boosting Classifier

The parameters for each classifier are tuned using sklearn’s grid search cross validation function with a precision_macro scoring. The scoring maximizes the tru positives and true negatives predicted by the model, making it more reliable.

Logistic Regression

log_reg = LogisticRegression(max_iter=1000)

params_log = {'C': [0.001, 0.01, 0.1, 1],

'penalty':['l2']}

log_gs = GridSearchCV(log_reg,

param_grid=params_log,

scoring='precision',

cv=5,

verbose=10,

n_jobs=-1)

log_gs.fit(X_sampled, y_sampled)

print("Best parameters found: ", log_gs.best_params_)

log_best = log_gs.best_estimator_

predictions_log = log_best.predict(X_test)

print(metrics.classification_report(y_test, predictions_log))

Fitting 5 folds for each of 4 candidates, totalling 20 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 8 concurrent workers.

[Parallel(n_jobs=-1)]: Done 2 tasks | elapsed: 16.0s

[Parallel(n_jobs=-1)]: Done 8 out of 20 | elapsed: 26.9s remaining: 40.3s

[Parallel(n_jobs=-1)]: Done 11 out of 20 | elapsed: 33.2s remaining: 27.2s

[Parallel(n_jobs=-1)]: Done 14 out of 20 | elapsed: 42.1s remaining: 18.1s

[Parallel(n_jobs=-1)]: Done 17 out of 20 | elapsed: 43.8s remaining: 7.7s

[Parallel(n_jobs=-1)]: Done 20 out of 20 | elapsed: 48.3s remaining: 0.0s

[Parallel(n_jobs=-1)]: Done 20 out of 20 | elapsed: 48.3s finished

/anaconda3/lib/python3.7/site-packages/sklearn/linear_model/logistic.py:432: FutureWarning: Default solver will be changed to 'lbfgs' in 0.22. Specify a solver to silence this warning.

FutureWarning)

Best parameters found: {'C': 0.01, 'penalty': 'l2'}

precision recall f1-score support

0 0.75 0.71 0.73 1684

1 0.41 0.46 0.43 737

accuracy 0.64 2421

macro avg 0.58 0.59 0.58 2421

weighted avg 0.65 0.64 0.64 2421

Linear SVM with L2 Regularization

lsvm = LinearSVC(max_iter=10000)

lsvm_param_grid = {'C': [1e-5, 1e-4, 1e-2]}

lsvm_gs = GridSearchCV(lsvm,

param_grid=lsvm_param_grid,

scoring='precision_macro',

cv=5,

verbose=1,

n_jobs=-1)

lsvm_gs.fit(X_sampled, y_sampled)

print("Best parameters found: ", lsvm_gs.best_params_)

lsvm_best = lsvm_gs.best_estimator_

predictions_lsvm = lsvm_best.predict(X_test.values)

print(metrics.classification_report(y_test, predictions_lsvm))

Fitting 5 folds for each of 3 candidates, totalling 15 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 8 concurrent workers.

[Parallel(n_jobs=-1)]: Done 15 out of 15 | elapsed: 3.6min finished

Best parameters found: {'C': 0.0001}

precision recall f1-score support

0 0.74 0.76 0.75 1684

1 0.42 0.39 0.40 737

accuracy 0.65 2421

macro avg 0.58 0.58 0.58 2421

weighted avg 0.64 0.65 0.64 2421

Random Forest

rf = RandomForestClassifier()

rf_param_grid = {'max_depth': range(8,11), 'n_estimators': range(100,201,20)}

rf_gs = GridSearchCV(rf,

param_grid=rf_param_grid,

scoring='precision_macro',

cv=5,

verbose=1,

n_jobs=-1)

rf_gs.fit(X_sampled, y_sampled)

print("Best parameters found: ", rf_gs.best_params_)

rf_best = rf_gs.best_estimator_

predictions_rf = rf_best.predict(X_test.values)

print(metrics.classification_report(y_test, predictions_rf))

Fitting 5 folds for each of 18 candidates, totalling 90 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 8 concurrent workers.

[Parallel(n_jobs=-1)]: Done 34 tasks | elapsed: 1.2min

[Parallel(n_jobs=-1)]: Done 90 out of 90 | elapsed: 3.3min finished

Best parameters found: {'max_depth': 10, 'n_estimators': 180}

precision recall f1-score support

0 0.73 0.79 0.76 1684

1 0.40 0.32 0.36 736

accuracy 0.65 2420

macro avg 0.56 0.56 0.56 2420

weighted avg 0.63 0.65 0.64 2420

Gradient Boosting

gb = GradientBoostingClassifier()

gb_param_grid = {'max_depth': range(8,11), 'n_estimators': range(100,201,20)}

gb_gs = GridSearchCV(gb,

param_grid=gb_param_grid,

scoring='precision_macro',

cv=5,

verbose=1,

n_jobs=-1)

gb_gs.fit(X_sampled, y_sampled)

print("Best parameters found: ", gb_gs.best_params_)

gb_best = gb_gs.best_estimator_

predictions_gb = gb_best.predict(X_test.values)

print(metrics.classification_report(y_test, predictions_gb))

Fitting 5 folds for each of 18 candidates, totalling 90 fits

[Parallel(n_jobs=-1)]: Using backend LokyBackend with 8 concurrent workers.

[Parallel(n_jobs=-1)]: Done 34 tasks | elapsed: 11.7min

[Parallel(n_jobs=-1)]: Done 90 out of 90 | elapsed: 37.6min finished

Best parameters found: {'max_depth': 10, 'n_estimators': 160}

precision recall f1-score support

0 0.71 0.78 0.75 1684

1 0.36 0.27 0.31 736

accuracy 0.63 2420

macro avg 0.53 0.53 0.53 2420

weighted avg 0.60 0.63 0.61 2420

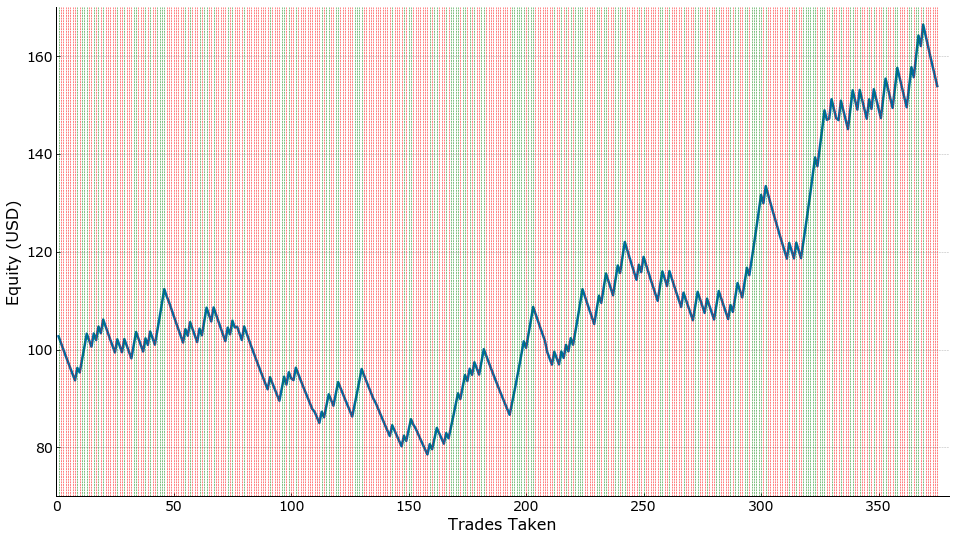

After identifying the best model, a trade simulation is run using the testing set. The estimated profit is calculated using the predictions and stoploss assumptions.

Results

The accuracy attained from all the models are below the heuristic target which is the significant PCC (1.25 x 54%) which is 67.8%. However, these results still beat the PCC and are still better than guessing trades at random. The effectiveness of this model could be further analyzed through the trade simulation.

Simulate trades using LSVM

Even if they both have a 65% accuracy, we choose Linear SVM over Random Forest as it has a better precision and recall for class 1.

pred_df = df.loc[testDATE:valiDATE]

pred_df['label'] = y_test

pred_df['pred'] = lsvm_best.predict(X_test)

pred_df.head()

| open | high | low | close | volume | ceiling | floor | ceiling2 | floor2 | boxnumber | ... | B4.1 | B5.1 | B6.1 | trigger | target100 | target150 | target200 | Unnamed: 46 | label | pred | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| datetime | |||||||||||||||||||||

| 2018-01-18 01:00:00 | 1326.71 | 1328.91 | 1326.71 | 1328.59 | 2199 | 1343.94 | 1325.97 | 1346.94 | 1322.97 | 6.73 | ... | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | 2018-01-18 | 0 | 0 |

| 2018-01-18 02:00:00 | 1328.57 | 1329.59 | 1327.45 | 1328.50 | 6744 | 1343.94 | 1325.97 | 1346.94 | 1322.97 | 6.73 | ... | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | 2018-01-18 | 0 | 0 |

| 2018-01-18 03:00:00 | 1328.52 | 1328.58 | 1324.27 | 1325.92 | 7417 | 1343.94 | 1325.97 | 1346.94 | 1322.97 | 6.73 | ... | 0.0 | 0.0 | 0.0 | -1.0 | NaN | NaN | NaN | 2018-01-18 | 0 | 0 |

| 2018-01-18 04:00:00 | 1325.92 | 1327.16 | 1325.88 | 1326.72 | 4356 | 1343.94 | 1325.97 | 1346.94 | 1322.97 | 6.73 | ... | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | 2018-01-18 | 1 | 1 |

| 2018-01-18 05:00:00 | 1326.69 | 1326.82 | 1325.26 | 1325.54 | 3512 | 1343.94 | 1325.97 | 1346.94 | 1322.97 | 6.73 | ... | 0.0 | 0.0 | 0.0 | 0.0 | NaN | NaN | NaN | 2018-01-18 | 0 | 0 |

5 rows × 48 columns

Simulation:

equity - this is the starting capital in thousands thus USD100,000

sl_threshold - is the stoploss which is an order to reduce the losses

equity = 100

sl_threshold = 1

committed = False

buy_price = 0

prediction = 0

hold_time = 0

bet = 0

target_price = 0

stop_loss = 0

trade_count = 0

equity_change = []

trade_results = []

delta_results = []

bet_list = []

target_list = []

buy_list = []

selling_list = []

time = []

sl_list = []

for _, hour in pred_df.iterrows():

if committed:

if hold_time < 4:

if hour.high >= target_price:

# win, sell current holdings

pip = (target_price - buy_price - 0.3)*100

equity += pip*bet

delta_results.append(pip*bet)

equity_change.append(equity)

selling_list.append(target_price)

trade_results.append(1)

committed = False

else:

# did not win yet, keep check stop_loss

if hour.low < stop_loss:

pip = (stop_loss - buy_price - .3)*100

equity += pip*bet

delta_results.append(pip*bet)

selling_list.append(stop_loss)

equity_change.append(equity)

trade_results.append(0)

committed = False

else:

hold_time += 1

else:

# lose, sell current holdings at open price

pip = (np.abs(hour.open - buy_price)-0.3)*100

equity -= pip*bet

delta_results.append(-pip*bet)

equity_change.append(equity)

selling_list.append(hour.open)

trade_results.append(0)

committed = False

else:

if hour.pred != 0:

trade_count += 1

committed = True

buy_price = hour.open

bet = equity/10000

bet_list.append(bet)

prediction = hour.pred

hold_time = 0

target_price = buy_price + 3

stop_loss = buy_price - sl_threshold

buy_list.append(buy_price)

target_list.append(target_price)

time.append(hour.name)

sl_list.append(stop_loss)

else:

committed = False

xcheck = pd.DataFrame(dict(buy=buy_list,

target=target_list,

stop_loss=sl_list,

sell=selling_list,

bet=bet_list,

delta=delta_results,

equity=equity_change), index=time)

xcheck

Sample Output

| buy | target | stop_loss | sell | bet | delta | equity | |

|---|---|---|---|---|---|---|---|

| 2018-01-18 04:00:00 | 1325.92 | 1328.92 | 1324.92 | 1328.92 | 0.010000 | 2.700000 | 102.700000 |

| 2018-01-18 16:00:00 | 1330.09 | 1333.09 | 1329.09 | 1329.09 | 0.010270 | -1.335100 | 101.364900 |

| 2018-01-18 18:00:00 | 1329.71 | 1332.71 | 1328.71 | 1328.71 | 0.010136 | -1.317744 | 100.047156 |

| 2018-01-19 04:00:00 | 1330.67 | 1333.67 | 1329.67 | 1329.67 | 0.010005 | -1.300613 | 98.746543 |

| 2018-01-19 12:00:00 | 1335.61 | 1338.61 | 1334.61 | 1334.61 | 0.009875 | -1.283705 | 97.462838 |

| 2018-01-19 16:00:00 | 1334.18 | 1337.18 | 1333.18 | 1333.18 | 0.009746 | -1.267017 | 96.195821 |

| 2018-01-22 13:00:00 | 1333.63 | 1336.63 | 1332.63 | 1332.63 | 0.009620 | -1.250546 | 94.945276 |

| 2018-01-23 15:00:00 | 1336.51 | 1339.51 | 1335.51 | 1335.51 | 0.009495 | -1.234289 | 93.710987 |

| 2018-01-23 17:00:00 | 1334.16 | 1337.16 | 1333.16 | 1337.16 | 0.009371 | 2.530197 | 96.241184 |

| 2018-01-24 03:00:00 | 1340.78 | 1343.78 | 1339.78 | 1342.05 | 0.009624 | -0.933539 | 95.307644 |

| 2018-01-24 11:00:00 | 1347.05 | 1350.05 | 1346.05 | 1350.05 | 0.009531 | 2.573306 | 97.880951 |

| 2018-01-24 13:00:00 | 1349.70 | 1352.70 | 1348.70 | 1352.70 | 0.009788 | 2.642786 | 100.523736 |

| 2018-01-24 16:00:00 | 1352.21 | 1355.21 | 1351.21 | 1355.21 | 0.010052 | 2.714141 | 103.237877 |

| 2018-01-25 10:00:00 | 1361.13 | 1364.13 | 1360.13 | 1360.13 | 0.010324 | -1.342092 | 101.895785 |

| 2018-01-25 16:00:00 | 1360.18 | 1363.18 | 1359.18 | 1359.18 | 0.010190 | -1.324645 | 100.571140 |

| 2018-01-25 18:00:00 | 1357.62 | 1360.62 | 1356.62 | 1360.62 | 0.010057 | 2.715421 | 103.286560 |

| 2018-01-25 22:00:00 | 1347.71 | 1350.71 | 1346.71 | 1346.71 | 0.010329 | -1.342725 | 101.943835 |

| 2018-01-26 03:00:00 | 1348.26 | 1351.26 | 1347.26 | 1351.26 | 0.010194 | 2.752484 | 104.696319 |

| 2018-01-26 11:00:00 | 1355.08 | 1358.08 | 1354.08 | 1354.08 | 0.010470 | -1.361052 | 103.335266 |

375 rows × 7 columns

fig, ax = plt.subplots(figsize=(16,9))

ax.plot(range(1, trade_count+1), equity_change)

ax.set_ylabel('Equity (USD)')

ax.set_xlabel('Trades Taken')

ax.grid(False)

ax.yaxis.grid(True)

ax.axis([0,380, 70, 170])

for i, tr in enumerate(trade_results):

if tr == 1:

ax.axvline(x=(i+1), c='g', ls='--', lw=0.5)

else:

ax.axvline(x=(i+1), c='r', ls='--', lw=0.5)

# ax.spines['left'].set_position(('data', 0))

Actual Simulation:

- target of 300 pips and a 100 stoploss

- period is from Jan 18, 2018 to Jun 15, 2018 or equivalent to six (6) months

- resulting profit is from USD100,000 to USD154,000 or an increase in capital by 54%

The predictions made from our model resulted in a total profit of \$53,855 (54% in 6 months). This is equivalent to an 8% month-on-month growth. These returns are within the average monthly returns of a professional forex trader which ranges between 1- 10% per month. It could also be observed that a larger portion of the trades caused losses which could be attributed to incorrect predictions. However, using the stop loss of 100 pips, the losses were still covered by the correct predictions.

Conclusion and Future Work

As some forex trading softwares allows scripting to automate their trades, it is entirely possible to retrain an updated model using latest 2019 data and other deep learning algorithms such as Long Short Term Memory to improve accuracy. These models can then be implemented for automated trading.

Forex trading also allows short selling which helps traders to earn from down trends. Therefore, the model could be further improved by converting it into a multinomial classifier. The model could then recommend no trade, trade (uptrend), and trade (downtrend). This would give more trading opportunities for the trader. Forex trading can be a better investment over stocks and fixed income for retailers. With the right strategy and discipline, an individual can gain profit of 1% with one trade per week and compounding it for 52 weeks in a year, it is equivalent to 66%.

Research Paper Available

The journal article can be accessed here.

Acknowledgements

This project was completed together with my learning teammates Lance Aven Sy and Janlo Cordero.